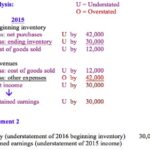

The result would give a far more accurate picture of the company’s true financial status. An investigation may determine that the company wrote a check for $20,000, which still needs to clear the bank. In this case, a $20,000 timing difference due to an outstanding check should be noted in the reconciliation. This insights and his love for researching SaaS products enables him to provide in-depth, fact-based software reviews to enable software buyers make better decisions.

In this article, you will learn everything you need to know about account reconciliation including how account reconciliation software works. As important as account reconciliation is in accounting, there is not much focus on it in accounting classes. In fact, many accountants can enjoy a successful career without having to perform a single account reconciliation.

The general ledger balance of an account is compared to independent systems, third-party data, or other supporting documentation to ensure the balance stated in the general ledger is extremely accurate. This process confirms that records of transactions are complete and consistent, helping companies make important business and financial decisions using very accurate records. And generating financial reports roles and responsibilities of a company shareholder in Clio Accounting is a breeze, making your life, and your accountant’s life that much easier.

Why is account reconciliation important?

- Most account reconciliations are performed against the general ledger, considered the master source of financial records for businesses.

- When account reconciliations are incorporated into the month-end closing process, this can delay the completion of the close.

- Take note that you may need to keep an eye out for transactions that may not match immediately between the sets of records for which you may need to make adjustments due to timing differences.

- After an investigation, the credit card is found to have been compromised by a criminal who was able to obtain the company’s information and charge the individual’s credit card.

Reconciliation in accounting—the process of comparing sets of records to check that they’re correct and in agreement—is essential for ensuring the accuracy of financial records for all kinds of businesses. For the legal profession, however, regular, effective reconciliation in accounting is key to maintaining both financial accuracy and legal compliance—especially when managing trust accounts. Reconciliation in accounting is not only important for businesses, but may also be convenient for households and individuals. It is prudent to reconcile credit card accounts and checkbooks on a regular basis, for example. This is done by comparing debit card receipts or check copies with a person’s bank statements.

Reconciliation for accounts receivable involves matching customer invoices and credits with aged accounts receivable journal entries. It makes sure that your customer account write-offs are correctly recorded against the Allowance for Doubtful Accounts and that discrepancies are addressed. Once data is gathered from these sources, the software, through advanced encoding, then compares account balances between documents from the different sources and identifies discrepancies. These are then investigated by publicrecordcenter com accounting staff to identify the main cause of the discrepancies. If there are any differences between the accounts and the amounts, these differences need to be explained.

How to reconcile balance sheet accounts

Reconciling your bank statements allows you to identify problems before they get out of hand. Because the individual is fastidious about keeping receipts, they call the credit card to dispute the amounts. After an investigation, the credit card is found to have been compromised by a criminal who was able to obtain the company’s information and charge the individual’s credit card. The individual is reimbursed for the incorrect charges, the card is canceled, and the fraudulent activity stopped.

These may be the result of billing mistakes related to loans, deposits, and payment processing activities. To implement effective reconciliation processes, you need to create and document the exact procedures that staff and lawyers should follow. Lastly, in the United States, account reconciliation is crucial to help companies comply with federal regulations applied by the Securities and Exchange Commission (SEC) under the Sarbanes-Oxley Act. An investigation may determine that the company recorded bank fees of $1,000 rather than $100. A $900 error should be noted during the reconciliation, and an adjusting journal entry should be recorded.

Vendor statements

Bank reconciliations sales journal: explanation format and example involve comparing the business’s financial statements with the statements it receives from the bank. This helps to ensure that the business’s records accurately reflect the transactions that have taken place in its bank account. Accounts payable reconciliation makes sure that general ledger balances match those in underlying subsidiary journals.

Check For Accurate and Consistent Balances

The balances between the two records must agree with each other, and any discrepancies should be explained in the account reconciliation statement. For lawyers, account reconciliation is particularly important when it comes to trust accounts. In fact, most jurisdictions have requirements for trust account reconciliation. For example, you may need to reconcile your trust account bank statement with client balances at a specific frequency, such as monthly or quarterly.